Date of Publication: May 18, 2026, 10:01 AM.

Updated On: May 18, 2026, 10:01 AM.

- Mergers & Acquisitions (M&A) viewed as primary growth strategy

- Monarch management identifies numerous lucrative opportunities

- The operator is often linked with acquisition talks, yet no deals finalized

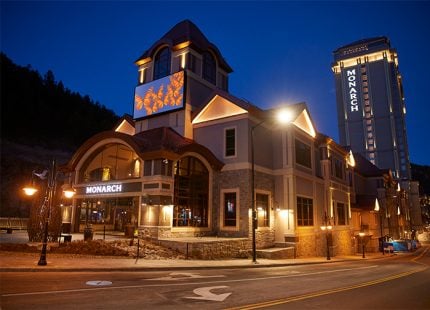

Monarch Casino & Resort (NASDAQ: MCRI) is a frequent candidate in discussions about potential acquisitions in the casino sector, and while they have yet to announce any deals, changes may be on the horizon.

David Katz, an analyst from Jefferies, recently engaged with the management team in Reno, concluding that mergers and acquisitions represent “the optimal path for growth,” noting that the current market presents a “highly appealing” landscape for Monarch to acquire new assets.

Management underscored that pinpointing the next stage of significant growth is their chief focus. Our meetings led us to believe that M&A emerges as the most probable strategy, though organic growth opportunities still exist, especially in Reno,” remarked Katz.

Operating only two casino hotels — the Atlantis in Reno and a property in Black Hawk, Colorado — Monarch is the smallest publicly traded casino operator in terms of properties. However, despite its limited portfolio, the stock has increased nearly 45% over the last year, showcasing solid performance in the market.

Opportune Time for Monarch Casino to Expand

Now may be a favorable time for Monarch to pursue acquisitions, as new regional gaming assets are predicted to emerge on the market soon.

Some analysts suggest that if Tilman Fertitta succeeds in acquiring Caesars Entertainment (NASDAQ: CZR), it may lead to a wave of regional casino sales due to the geographic overlap between Caesars and Fertitta’s Golden Nugget.

There’s a possibility that regulators in some of the eight states where both Caesars and Golden Nugget operate may compel divestitures, creating a favorable scenario for interested buyers. While it’s uncertain if Caesars will change hands, the potential for asset sales could present attractive opportunities for Monarch, whose executives are evidently contemplating new deals.

“Management perceives that the pool of external growth opportunities is broader than it has been in the last five years,” states Katz. “The desired acquisition profile includes properties that have stable real estate and are located in a thriving economy with a favorable regulatory atmosphere.”

Katz recommends a “hold” rating for the stock with a target price of $113.

Monarch Casino Will Exercise Caution

Investors who are acquainted with Monarch understand two key points about any potential consolidation strategy. First, management will not pursue an acquisition merely for the sake of expansion. Second, there’s a rigorous set of criteria that any prospective targets must fulfill.

For instance, Monarch is likely to focus on targets that include real estate in the negotiation, and as Katz notes, the operator is expected to prioritize markets “characterized by population growth, competitive dynamics, tax stability, and fair pricing.”

While these rigorous standards may limit the pool of potential targets for Monarch, this meticulous approach ultimately benefits investors, as evidenced by the previously mentioned increase in share price.